Cash Envelope System for Beginners: A Step-by-Step Guide to Finally Take Control of Your Money

You’ve probably heard people talk about the cash envelope system and thought — really? Actual cash? In 2025?

But here’s the truth: if you’ve been struggling to stick to a budget, overspending on groceries, or just feeling like your paycheck disappears before the month is over, this old-school method might be exactly what you need.

The cash envelope system is one of the most beginner-friendly ways to budget. It’s simple, visual, and — most importantly — it works. Whether you’re earning $1,200 or $2,000 a month, this system can help you spend with intention, stop leaking money, and even start building a small emergency fund.

In this guide, you’ll learn exactly how to start the cash envelope system from scratch. No complicated spreadsheets. No confusing finance apps. Just a few envelopes and a plan.

What Is the Cash Envelope System?

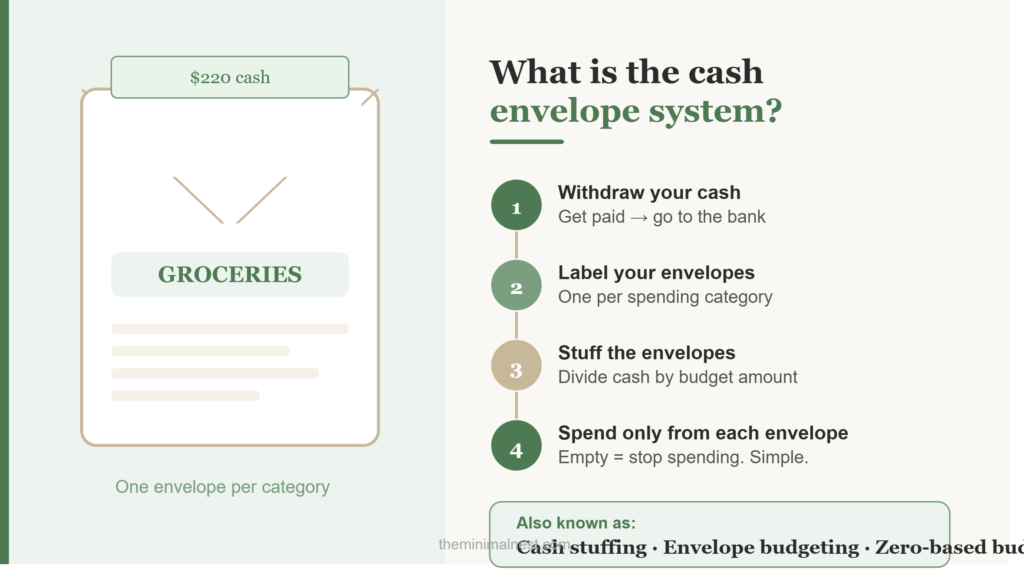

At its core, the cash envelope system is exactly what it sounds like. You take your income, divide it into spending categories, withdraw the cash, and put it into labeled envelopes.

Each envelope represents a category — groceries, gas, dining out, clothing. Once the money in that envelope is gone, you stop spending in that category until next month. No swiping a card and forgetting about it. Just real, tangible money you can see running out.

This method is sometimes called cash stuffing — a popular trend on Pinterest and YouTube where people show themselves filling envelopes as part of their budgeting routine. And while it looks aesthetically pleasing on camera, it’s also surprisingly effective at getting your finances under control.

The cash envelope system is a physical budgeting method where you divide your monthly cash into labeled envelopes — one for each spending category. When an envelope is empty, spending in that category stops. It helps beginners control variable expenses and avoid overspending, especially on a low or fixed income.

How It Works — At a Glance

- Withdraw your monthly or bi-weekly cash in full

- Label one envelope per spending category

- Fill each envelope with the budgeted amount

- Spend only what’s in each envelope

- Track what’s left at the end of the month

- Adjust amounts for next month based on real spending

Why the Cash Envelope System Works (Especially on a Low Income)

The reason most budgets fail isn’t lack of willpower — it’s lack of visibility. When you pay with a card, you’re spending abstract numbers. When you pay with cash, you’re spending something real.

Research shows that people experience more “pain of paying” with physical cash than with credit or debit cards. That emotional friction is actually a good thing when you’re trying to stick to a budget. Studies have found people spend 12–18% more when using cards versus cash.

For anyone budgeting on under $2,000 a month, this matters even more. Every dollar has a job. Every envelope keeps you accountable. And when you can physically see your grocery envelope getting thin, you start making smarter choices at the store.

Benefits of the Cash Envelope System

- Stops mindless overspending — instantly

- Makes budgeting visual and tangible

- Works without apps, internet, or a smartphone

- Helps you practice zero-based budgeting naturally

- Great for variable expenses that are hard to track digitally

- Builds the habit of intentional spending

- Encourages saving even on a very low income

78% of Americans live paycheck to paycheck (LendingClub, 2024). Only 32% maintain a household budget (Gallup). The cash envelope system is one of the simplest ways to break both of those statistics.

What You Need to Get Started

The beauty of this system is that you don’t need much. In fact, the supplies cost almost nothing and are available anywhere.

Basic Supplies Checklist

- A set of envelopes (plain manila or decorative cash envelopes)

- A pen or marker to label them

- A budget worksheet or notebook

- Access to your bank to withdraw cash

- Your monthly take-home income number

- About 30 minutes to set everything up

That’s really it. You don’t need a fancy wallet system on day one. Start simple — you can always upgrade to a cash envelope binder or accordion wallet later if you want something more organized.

Optional Upgrade: Cash Envelope Setup Comparison

| Option | Cost | Best For |

|---|---|---|

| Plain Envelopes + Pen | Under $2 | Absolute beginners testing the system |

| Decorative Cash Envelopes | $5–$15 | Those who want visual motivation |

| Clear Zip Pouches | $8–$15 | Neat organizers, see-through preference |

| Cash Envelope Wallet / Binder | $15–$35 | Long-term users, frequent spenders |

| Full Binder System | $25–$50 | Power budgeters, multiple income streams |

(Add your Amazon Associates links here for: cash envelope wallet, budget planner notebook, clear zip pouches, and The Total Money Makeover by Dave Ramsey)

Step-by-Step: How to Start the Cash Envelope System

Ready to get started? Follow these steps in order. Don’t skip ahead — especially if this is your first time budgeting.

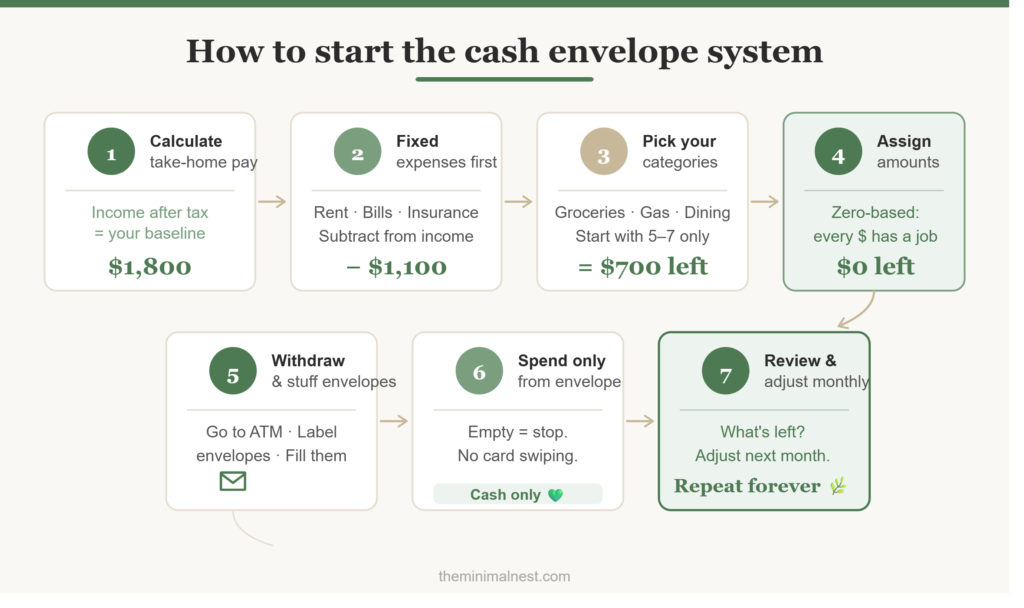

Write down exactly how much money comes in each month after taxes. If your income varies, use your lowest month as your baseline — it’s always better to budget conservatively.

Fixed expenses cost the same every month — rent, utilities, insurance, phone, minimum debt payments. Write them all down and subtract them from your income.

Variable expenses change month to month — groceries, gas, dining out, clothing, entertainment. These are the categories that go in envelopes, because they’re where most people leak money.

This is where zero-based budgeting comes in. Every dollar of your remaining money gets assigned to an envelope. No dollars left unaccounted for.

Go to your bank or ATM and withdraw the exact amounts you’ve budgeted. Label your envelopes and stuff them. Do this at the start of every pay period.

When you go grocery shopping, bring only your grocery envelope. Pay with that cash. Whatever’s left stays in the envelope until next month. If an envelope runs out, you stop spending — or consciously move money from a lower-priority envelope.

Look at what’s left in each envelope. Grocery envelope always empty by week three? Bump it up. Entertainment always has $30 left? Redirect that to your emergency fund. Your budget improves by learning your own patterns.

How to Set Up Your Envelope Categories

Not sure how many envelopes you need or how to name them? Here’s a practical guide. Start with 5–7 envelopes maximum — too many categories leads to confusion and burnout.

| Envelope Category | Suggested % of Remaining | Notes |

|---|---|---|

| 🛒 Groceries | 30–35% | Your most important envelope |

| ⛽ Gas / Transport | 10–12% | Adjust based on your commute |

| 🍜 Dining Out | 7–9% | Treat this as a fun splurge envelope |

| 🧹 Household Supplies | 6–8% | Cleaning, paper goods, etc. |

| 💇 Personal Care | 4–5% | Haircuts, toiletries, skincare |

| 👗 Clothing | 4–5% | Optional; reduce in tight months |

| 🎬 Entertainment | 5–7% | Movies, hobbies, small fun budget |

| 🆘 Emergency Fund | 10–15% | Non-negotiable — save this first |

| 🎲 Miscellaneous | 5–7% | Buffer for random expenses |

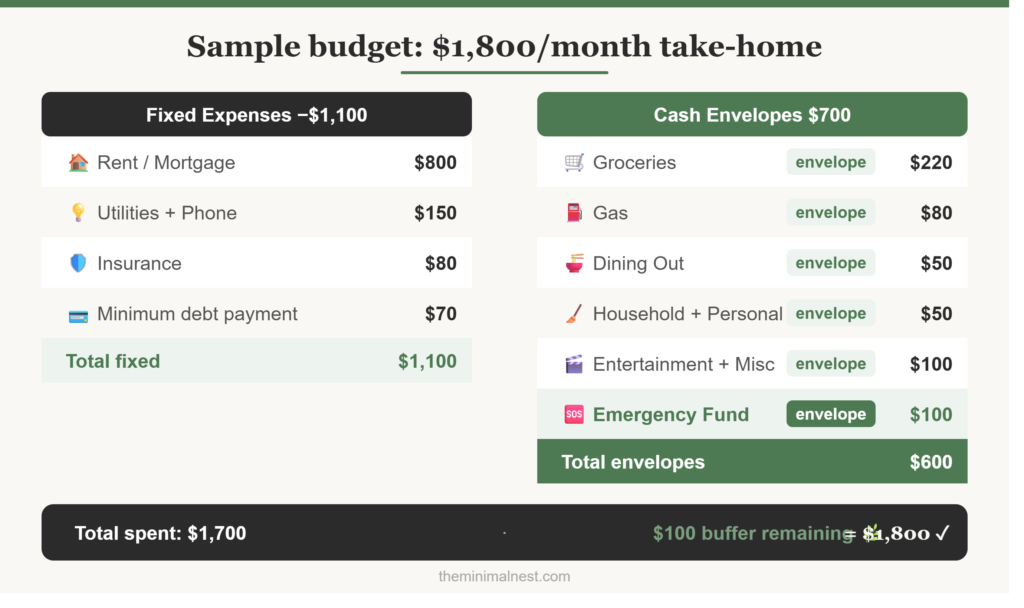

Cash Envelope System on Under $2,000 a Month

If you’re budgeting on a low income, the cash envelope system isn’t just helpful — it’s a lifeline. Here’s a real-world example of how to make it work on $1,800/month take-home pay.

| Category | Type | Monthly Amount |

|---|---|---|

| 🏠 Rent / Mortgage | Fixed | $800 |

| 💡 Utilities + Phone | Fixed | $150 |

| 🛡️ Insurance | Fixed | $80 |

| 💳 Minimum Debt Payment | Fixed | $70 |

| 🛒 Groceries (envelope) | Variable | $220 |

| ⛽ Gas (envelope) | Variable | $80 |

| 🍜 Dining Out (envelope) | Variable | $50 |

| 🧹 Household + Personal (envelope) | Variable | $50 |

| 🆘 Emergency Fund (envelope) | Variable | $100 |

| 🎬 Entertainment + Misc (envelope) | Variable | $100 |

| ✅ TOTAL | $1,700 (keeps $100 buffer) |

When you’re on a tight income, a small buffer prevents overdraft from one unexpected charge. And notice the emergency fund envelope — even $100/month adds up to $1,200 in a year. That’s a real emergency fund that could cover a car repair, a medical copay, or a month with reduced hours.

One-Income Household Tips

- Budget the moment your paycheck deposits — not a few days later

- Keep a ‘buffer’ envelope with $50–$100 for genuine surprises

- Review your budget every Sunday to stay aware of what’s left

- Don’t use the emergency fund envelope for non-emergencies

- If income fluctuates, always build your budget around your lowest monthly income

Common Mistakes Beginners Make (And How to Avoid Them)

The cash envelope system is simple, but not mistake-proof. Here are the most common issues and how to sidestep them.

❌ Mistake #1: Starting With Too Many Envelopes

More isn’t always better. If you start with 15 envelopes, you’ll spend more time managing the system than using it. Begin with 5–7 and add more later.

❌ Mistake #2: Not Adjusting After the First Month

Your first month is a learning experiment. Most beginners underestimate grocery spending and overestimate how little they spend dining out. Review and adjust — that’s part of the process.

❌ Mistake #3: “Borrowing” From Other Envelopes Without a Rule

Moving money between envelopes is allowed — but only intentionally. A good rule: you can borrow from entertainment before groceries, never the other way around.

❌ Mistake #4: Forgetting Irregular Expenses

Car registration, doctor’s visits, birthday gifts — these pop up a few times a year. Create a “Sinking Funds” envelope and set aside $20–$30/month toward it.

❌ Mistake #5: Giving Up After One Rough Month

Budgeting is a skill, not a talent. The people who succeed with cash envelopes aren’t more disciplined — they’re just more patient with themselves during the learning curve.

Personal finance experts like Dave Ramsey have long advocated for cash-based budgeting as the fastest way to stop overspending. The psychological impact of physical money creates a real spending “brake” that digital payments don’t provide. If you’ve tried apps or spreadsheets without success, commit to cash for just 30 days.

Tips to Make the Cash Envelope System Stick Long-Term

Getting started is the easy part. Staying consistent is where most people struggle. Here’s what actually helps.

- Make envelope-filling a monthly ritual — put on music, light a candle, make it calm

- Keep your envelopes somewhere visible (a wallet, a binder, a spot on your desk)

- Review your budget every Sunday to stay aware of what’s left

- Celebrate small wins — leftover money in your dining envelope? That’s a real win

- Tell a trusted friend or partner about your budget for accountability

- Give yourself one guilt-free envelope with a small amount just for fun

The cash envelope system works best when it doesn’t feel like punishment. Keep it flexible enough to live your life, but structured enough to move your finances forward. Minimalism and budgeting go hand in hand — both are about spending with intention, not restriction.

Frequently Asked Questions

What is the cash envelope system in simple terms?

It’s a budgeting method where you divide your cash into labeled envelopes, one per spending category. You can only spend what’s in each envelope. When it’s empty, you stop spending in that category until next month.

Can the cash envelope system work on a low income?

Yes — it works especially well on a low income because it forces you to prioritize. When you have $1,500 or $1,800/month, every dollar matters. The envelope system makes those dollars visible and harder to waste.

How many envelopes do I need as a beginner?

Start with 5 to 7 envelopes. Common starter envelopes: groceries, gas, dining out, personal care, entertainment, household, and emergency fund. Too many categories overwhelm beginners.

What do I do with leftover cash at the end of the month?

You have options: roll it into next month’s same envelope, move it to your emergency fund, or use it as a small reward. Most minimalist budgeters recommend rolling leftover cash into savings.

Can I still use a debit card with the cash envelope system?

The system works best with physical cash. However, you can use a digital hybrid — tracking category spending in a spreadsheet and treating each budget as a virtual envelope. Research still shows physical cash leads to better spending control.

What is zero-based budgeting and how does it relate?

Zero-based budgeting means every dollar of your income gets assigned a purpose — expenses, savings, or debt payments — until you reach zero. The cash envelope system is the physical, hands-on version of zero-based budgeting applied to variable spending categories.

What if I run out of cash in an envelope before the month ends?

You can stop spending in that category until next month, borrow from a lower-priority envelope with intention, or note that you need to increase that envelope’s budget next month. Running out is actually useful data — it tells you where your real spending lies.

How do I handle online shopping or bills with the cash envelope system?

Fixed bills like rent, utilities, and subscriptions are paid from your bank account as normal — they don’t go in envelopes. Envelopes are for variable, in-person spending where you’re most likely to overspend. For online shopping, transfer the exact budgeted amount to a dedicated card or track it as a virtual envelope.

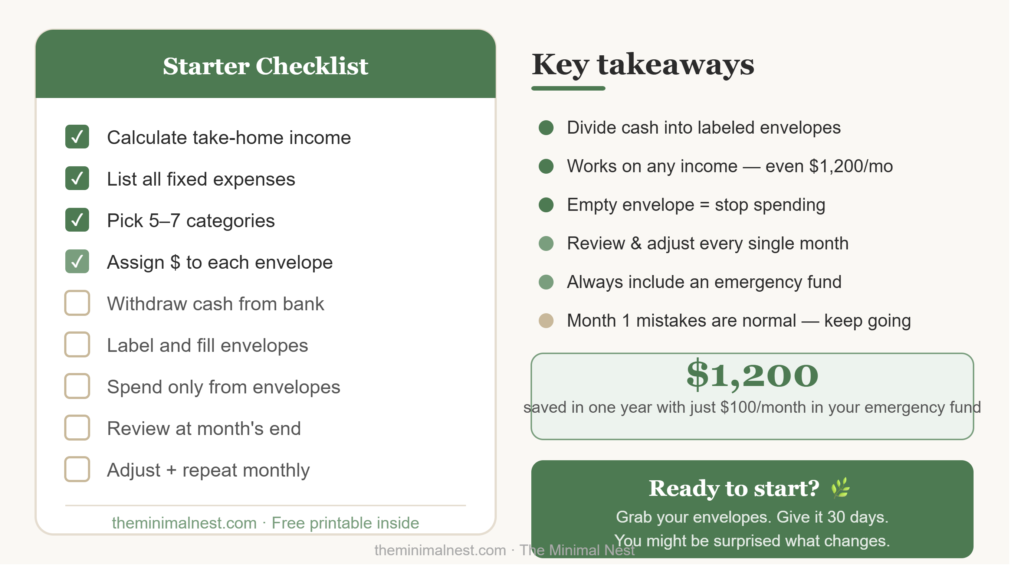

- The cash envelope system divides your spending money into labeled physical envelopes by category

- It works on any income — even under $2,000/month — because it forces conscious spending

- Start with just 5–7 envelopes to keep it simple and sustainable

- Withdraw cash at the start of each pay period and fill your envelopes immediately

- When an envelope is empty, stop spending in that category — that’s the whole point

- Review and adjust your budget amounts at the end of every month

- Always include an emergency fund envelope, even if it’s just $50/month

- Mistakes in the first month are normal — keep going anyway

🗒️ Beginner Checklist: Start the Cash Envelope System Today

- Calculate your monthly take-home income

- List and total all fixed expenses

- Identify 5–7 variable spending categories

- Assign a dollar amount to each category

- Withdraw cash from your bank

- Label and fill your envelopes

- Spend only from the envelopes this month

- Review what’s left at month’s end

- Adjust amounts for next month

- Repeat — consistency is the secret

Final Thoughts

The cash envelope system isn’t flashy. It isn’t an app. It doesn’t require a finance degree or a high salary to use. It’s just you, your money, and a few envelopes — and that simplicity is exactly why it works.

If you’ve been stuck in a cycle of overspending, wondering where your paycheck went, or too anxious to even look at your bank account, this system gives you a way out. One envelope at a time.

Start small. Start imperfect. Start this month.

Grab a few envelopes, write down your categories, and give it 30 days. You might be surprised what changes when you actually see and feel your money.

Ready to Take Control of Your Money? 🌿

Have you tried the cash envelope system? Drop a comment below and let me know which category surprised you the most! And don’t forget to save this post to Pinterest so you can come back to it anytime.

Explore More Money Tips →You Might Also Like

Discover the core differences and which lifestyle suits you best.

Spend less, stress less, and build real wealth with minimalist money habits.